- Scotiabank

- National Bank

- RBC

- CIBC

- BMO

- TD

From RBC to TD, Canada’s major banks posted fourth-quarter earnings this week, highlighting shifting profits, credit trends, and signals for investors. The post Stock news for investors: Fourth-quarter earnings roll in from Canada’s big banks appeared first on MoneySense.From RBC to TD, Canada’s major banks posted fourth-quarter earnings this week, highlighting shifting profits, credit trends, and signals for investors. The post Stock news for investors: Fourth-quarter earnings roll in from Canada’s big banks appeared first on MoneySense.

Stock news for investors: Fourth-quarter earnings roll in from Canada’s big banks

Featured RRSP Accounts

featured

EQ Bank

Build your retirement savings with 1.50% interest, tax-deferred contributions and zero fees.

go to site

featured

Registered GIC rate

Earn a guaranteed 2.75% in your RRSP when you lock in for 1 year.

go to site

Best RRSP rates

See our ranking of the best RRSP accounts and rates available in Canada.

read now

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

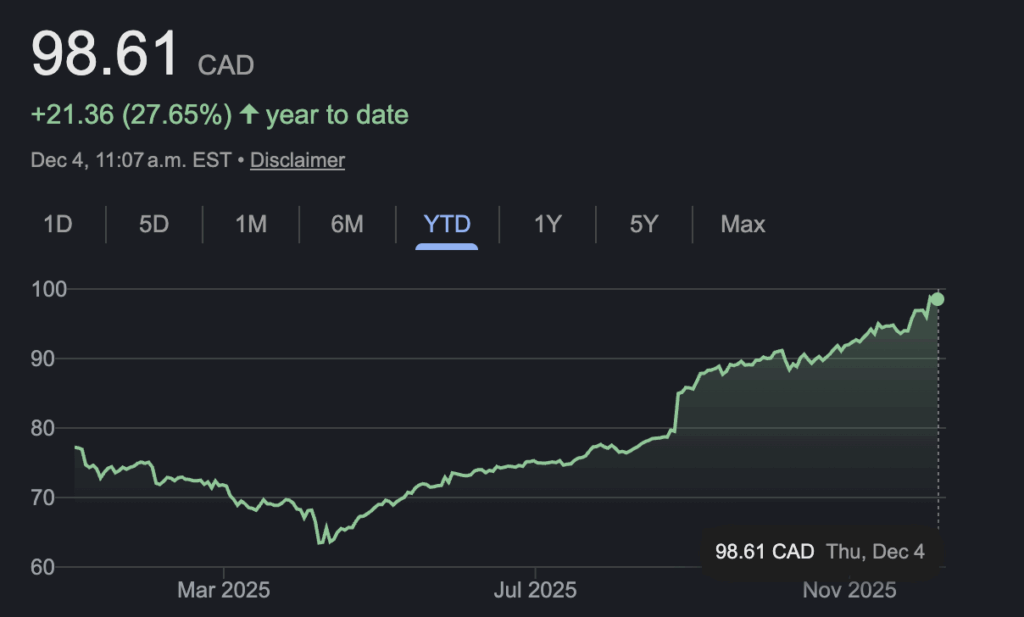

Scotiabank reports $2.21B Q4 profit up from $1.69B a year ago

Scotiabank (TSX:BNS)

Numbers for its fourth quarter:

- Profit: $2.21 billion (up from $1.69 billion a year ago)

- Revenue: $9.80 billion (up from $8.53 billion)

Scotiabank says it earned $2.21 billion in net income for its fourth quarter, up from $1.69 billion in the same quarter last year, helped by strength in its wealth management and capital markets businesses. The bank said Tuesday the profit amounted to $1.65 per diluted share for the quarter ended Oct. 31, up from $1.22 per diluted share in the same period a year ago.

Revenue totalled $9.80 billion, up from $8.53 billion in the same quarter last year. The bank’s provision for credit losses amounted to $1.11 billion for the quarter, up from $1.03 billion a year ago.

On an adjusted basis, Scotiabank says it earned $1.93 per diluted share in its latest quarter, up from an adjusted profit of $1.57 per diluted share a year ago. Analysts on average had expected an adjusted profit of $1.84, according to estimates compiled by LSEG Data & Analytics.

Scotiabank chief executive Scott Thomson said 2025 was a very positive year for the bank. “We delivered improving results through the year as we strengthened our balance sheet, improved our loan-to-deposit ratio, and increased return on equity,” Thomson said in a statement. “This quarter all our business lines reported year-over-year earnings growth with particular strength in global wealth management and global banking and markets and improving results in Canadian banking.”

The bank’s global wealth management business earned $447 million in net income attributable to equity holders, up from $380 million in the same quarter last year, while its global banking and markets business earned $519 million for the quarter, up from $347 million a year ago.

Scotiabank’s Canadian banking operations earned $941 million in its latest quarter, up from $934 million in the same quarter last year. Meanwhile, Scotiabank’s international banking arm earned $634 million in net income attributable to equity holders of the bank for the quarter, up from $600 million a year ago.

Source Google

Source Google

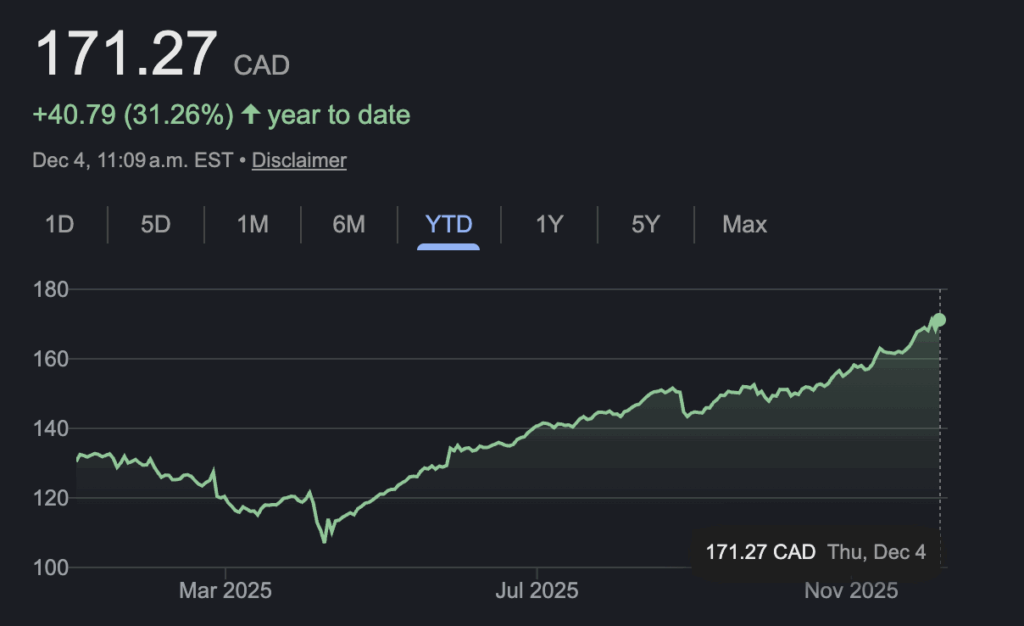

National Bank reports $1.06B fourth-quarter profit, raises dividend

National Bank of Canada (TSX:NA)

Numbers for its fourth quarter:

- Profit: $1.06 billion (up from $955 million a year ago)

- Revenue: $3.70 billion (up from $2.94 billion)

National Bank of Canada raised its dividend as it reported a fourth-quarter profit of $1.06 billion. The bank said Wednesday it will now pay a quarterly dividend of $1.24 per share, an increase of six cents.

National Bank, which announced Tuesday that it was buying Laurentian Bank’s retail and small business segments, says its fourth-quarter profit amounted to $2.57 per diluted share, compared with net income of $955 million or $2.66 per diluted share a year ago when it had fewer shares outstanding.

Revenue for the quarter ended Oct. 31 totalled $3.70 billion, up from $2.94 billion a year earlier.

The bank’s provisions for credit losses amounted to $244 million, up from $162 million in the same quarter last year. On an adjusted basis, National Bank says it earned $2.82 per diluted share in its latest quarter, up from an adjusted profit of $2.58 per diluted share in the same quarter last year. Analysts on average had expected an adjusted profit of $2.62 per share, according to estimates compiled by LSEG Data & Analytics.

“With our strengthened national presence, diversified business mix, strong capital ratios and prudent credit profile, we are well-positioned to generate continued growth and superior returns, in what will remain a complex macro-environment,” National Bank chief executive Laurent Ferreira said in a statement.

The bank said its personal and commercial banking group earned $319 million in its latest quarter, down from $327 million a year ago, as it was hit by costs related to the acquisition of Canadian Western Bank.

National Bank’s wealth management business earned $258 million, up from $219 million, while its capital markets arm earned $432 million, up from $306 million.

National Bank’s U.S. specialty finance and international operations earned $174 million, up from $157 million in the same quarter last year.

Source Google

Source Google

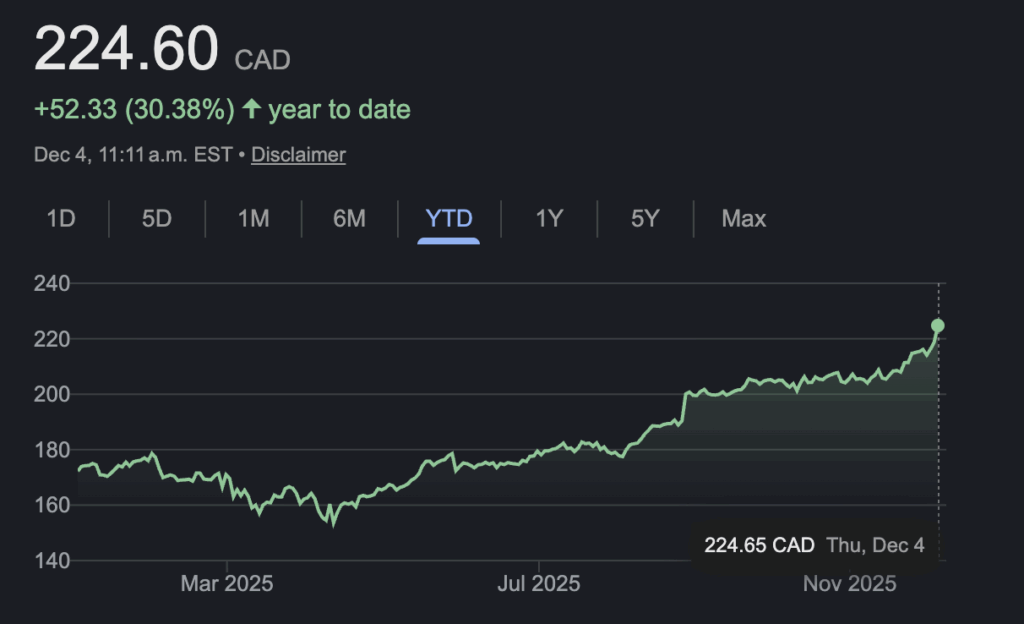

RBC posts record Q4 profit but CEO raises concerns about uneven economic recovery

Royal Bank of Canada (TSX:RY)

Numbers for its fourth quarter:

- Profit: $5.43 billion (up from $4.22 billion a year ago)

- Revenue: $17.21 billion (up from $15.07 billion)

Royal Bank of Canada handily beat analyst expectations as it reported record fourth-quarter results that showed rising profits across most divisions.

The bank said Wednesday it made a profit of $5.43 billion in the quarter ending Oct. 31, up from a profit of $4.22 billion a year ago, as capital markets, wealth management and personal and commercial banking all saw higher returns, offset by lower results in insurance. The results helped lead RBC to increase its quarterly dividend to $1.64 per share, up from $1.54 per share.

The bank sees continued strength ahead, raising its return-on-equity target to 17 per cent, up from 16 per cent.

RBC’s results and outlook come despite continued trade and economic uncertainty, but chief executive Dave McKay expressed cautious optimism on the wider picture. “While the operating environment remains fluid and complex, and there is a lot of hard work yet to be done by governments and the private sector, I am cautiously optimistic on the outlook for Canada,” he said on an earnings call with analysts Wednesday.

McKay noted that overall Canada’s effective tariff rate remains low and has done little to impact exports to the U.S., while the ongoing shift to a service-oriented economy should also offset some trade-related headwinds. He did, however, express concern with the split economic recovery, which is leading to increased inequality.

“The impact of the K-shaped economy is increasingly polarizing, with more affluent consumers investing disposable income and growing markets, while less affluent consumers struggle with affordability.” The trend can be seen in RBC’s own results, with its capital markets and wealth management divisions driving much of the earnings beat.

Meanwhile, many borrowers continue to struggle, with the bank increasing its provisions for potentially bad loans in the quarter to $1.01 billion, up from $840 million a year ago.

Chief risk officer Graeme Hepworth said the overall Canadian economy has demonstrated strong resilience this past year with household spending strong, but the bank has maintained a prudent approach to provisions given trade issues are largely unresolved and pockets of concern remain.

“Rising unemployment in Ontario and the Greater Toronto Area, coupled with higher payments at mortgage renewal, have contributed to rising consumer impairments in these regions,” said Hepworth. “We expect retail losses to remain elevated in 2026 as we work through the lag effect of higher unemployment, consumer insolvencies, and ongoing payment shocks for mortgage renewals in Canada.”

The areas of concern did little to hold back overall results, with adjusted earnings of $3.85 per diluted share in the quarter, up from an adjusted profit of $3.07 per diluted share in the same quarter last year.

Analysts on average had expected an adjusted profit of $3.53 per share, according to estimates compiled by LSEG Data & Analytics.

Scotiabank analyst Mike Rizvanovic said that while credit losses were elevated, they remained manageable as other areas like capital markets and wealth shined. “A strong quarter overall for (Royal Bank) at first look, driven by outsized growth in the top line that benefited once again from solid gains in market-sensitive businesses, which comfortably offset a modest miss across other business lines,” he said in a note.

Revenue totalled $17.21 billion, up from $15.07 billion in the same quarter last year.

RBC’s wealth management arm earned $1.28 billion, up from $969 million a year ago, while the bank’s capital markets business earned $1.43 billion, up from $985 million in the same quarter last year. Personal banking earned $1.89 billion in the bank’s latest quarter, up from $1.58 billion a year ago. Commercial banking operations earned $810 million, up from $774 million. RBC’s insurance business earned $98 million, down from $162 million a year ago.

Source Google

Source Google

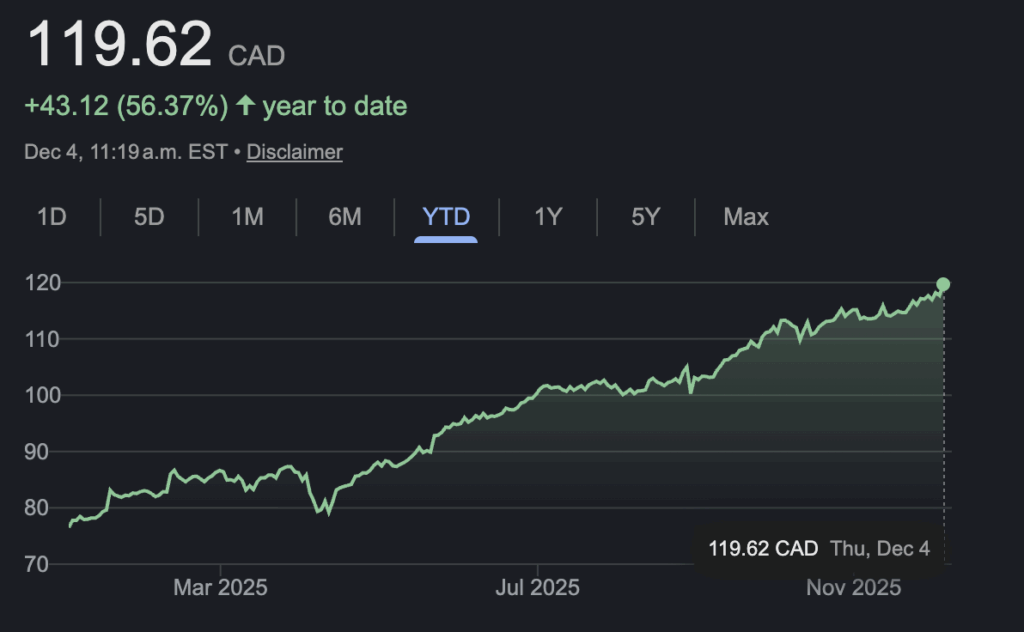

CIBC reports fourth-quarter profit up from year ago, raises dividend

CIBC (TSX:CM)

Numbers for its fourth quarter:

- Profit: $2.18 billion (up from $1.88 billion a year ago)

- Revenue: $7.58 billion (up from $6.62 billion)

CIBC raised its dividend as it reported a fourth-quarter profit of $2.18 billion, up from $1.88 billion a year ago. The bank said Thursday it will now pay a quarterly dividend of $1.07 per share, up from 97 cents per share. CIBC says its profit for the quarter ended Oct. 31 amounted to $2.20 per diluted share, up from $1.90 per diluted share a year ago.

Revenue for the quarter totalled $7.58 billion, up from $6.62 billion, while the bank’s provision for credit losses amounted to $605 million, up from $419 million a year ago. On an adjusted basis, CIBC says it earned $2.21 per diluted share, up from an adjusted profit of $1.91 per diluted share in the same quarter last year.

Analysts on average had expected an adjusted profit of $2.08 per share, according to estimates compiled by LSEG Data & Analytics.

“In a dynamic operating environment, our proactive and disciplined approach to managing our business, our resilient capital position and our deep client relationships supported robust growth while maintaining strong credit quality,” CIBC chief executive Harry Culham said in a statement.

CIBC said the growth came as its Canadian personal and business banking business earned $796 million in its latest quarter, up from $792 million a year ago as higher revenue was partially offset by a higher provision for credit losses and higher expenses.

The bank’s Canadian commercial banking and wealth management group earned $603 million, up from $551 million a year ago, while its U.S. commercial banking and wealth management business earned $275 million, up from $200 million a year ago.

CIBC’s capital markets business earned $548 million, up from $346 million in the same quarter last year.

CIBC also announced several senior executive changes Thursday that will be effective Jan. 1. The bank said Sandy Sharman, senior executive vice-president and group head, people, culture and brand, will transition to the role of special adviser before retiring at the end of 2026. CIBC also said Christina Kramer, senior executive vice-president and chief administrative officer, will add responsibility for enterprise real estate, enterprise capabilities and organizational agility, brand, community investment, client experience, communications, and corporate events. Richard Jardim will be appointed senior executive vice-president and chief technology and information officer, global technology, data and AI, while Yvonne Dimitroff will become executive vice-president and chief human resources officer, people, culture and talent.

Source Google

Source Google

BMO Financial Group reports $2.3B fourth-quarter profit, raises dividend

BMO Financial Group (TSX:BMO)

Numbers for its fourth quarter:

- Profit: $2.30 billion (compared to $2.30 billion a year ago)

- Revenue: $9.34 billion (up from $8.96 billion)

BMO Financial Group raised its dividend as it reported a fourth-quarter profit of $2.30 billion. The bank said Thursday it will now pay a quarterly dividend of $1.67 per share, an increase of four cents per share. BMO says its profit amounted to $2.97 per diluted share for the quarter ended Oct. 31 compared with a profit of $2.30 billion or $2.94 per diluted share a year ago when it had more shares outstanding.

Revenue for the quarter totalled $9.34 billion, up from $8.96 billion last year, while the bank’s provision for credit losses totalled $755 million, down from $1.52 billion a year ago. On an adjusted basis, BMO says it earned $3.28 per diluted share, up from an adjusted profit of $1.90 per diluted in the same quarter last year.

Analysts on average had expected an adjusted profit of $3.03 per share, according to estimates compiled by LSEG Data & Analytics.

“Fiscal 2025 was a strong year for BMO, with consistent execution and growing momentum to achieve our commitments to shareholders,” BMO chief executive Darryl White said. “We enter 2026 in a position of financial strength, with a focused strategy and a winning culture that continues to grow and attract talent across the bank.”

BMO said its Canadian personal and commercial banking business earned $752 million, up from $750 million a year ago, while its U.S. banking business earned $807 million, up from $281 million in the same quarter last year.

The bank’s wealth management arm earned $383 million, up from $301 million a year ago.

BMO’s capital markets business earned $521 million, up from $251 million in the same quarter last year.

The bank also announced Thursday the appointment of Tammy Brown to its board of directors.

Brown previously served as deputy chair of KPMG Canada’s board of directors and was a partner and national industry leader for industrial markets at the firm.

Source Google

Source Google

TD Bank reports $3.28B fourth-quarter profit, raises dividend

TD Bank Group (TSX:TD)

Numbers for its fourth quarter:

- Profit: $3.28 billion (down from $3.64 billion a year ago)

- Revenue: $15.49 billion (down from $15.51 billion)

TD Bank Group raised its dividend as it reported its fourth-quarter profit fell compared with a year ago, weighed down by one-time restructuring charges. The bank said Thursday it will pay a quarterly dividend of $1.08 per share, up from $1.05 per share.

TD says its profit amounted to $3.28 billion or $1.82 per diluted share for the quarter ended Oct. 31, compared with a profit of $3.64 billion or $1.97 per diluted share a year ago. On an adjusted basis, TD says it earned $2.18 per diluted share for its latest quarter, up from an adjusted profit of $1.72 per diluted share in the same quarter last year.

Revenue for the quarter totalled $15.49 billion, down from $15.51 billion a year ago, while the bank’s provision for credit losses amounted to $982 million, down from $1.11 billion in the same quarter last year.

Analysts on average had expected an adjusted profit of $2.03 per share, according to estimates compiled by LSEG Data & Analytics.

“TD had a strong fourth quarter, delivering robust fee and trading income in our markets-driven businesses as well as volume growth year-over-year in Canadian personal and commercial banking, capping a year of strong performance,” TD chief executive Raymond Chun said in a statement.

TD said its Canadian personal and commercial banking business earned $1.87 billion in its latest quarter, up from $1.82 billion a year ago as higher revenue was partially offset by higher provisions for credit losses and non-interest expenses.

The bank’s U.S. retail banking operations earned $719 million, up from $702 million in the same quarter last year.

TD’s wealth management business earned $699 million in the quarter, up from $349 million a year ago, while the bank’s wholesale baking group earned $494 million, up from $235 million in the same quarter last year.

Source Google

Source Google

Tools

MoneySense’s ETF Screener Tool

use tool

Read more news:

- News for investors: Barrick settles Mali dispute and Couche-Tard profit climbs

- Canadians aren’t as generous as they used to be

- Credit counselling calls surge as Canadians struggle with rising costs

- How cash ETFs keep your money working

The post Stock news for investors: Fourth-quarter earnings roll in from Canada’s big banks appeared first on MoneySense.

Piyasa Fırsatı

Rubic Fiyatı(RBC)

$0.005036

$0.005036$0.005036

USD

Rubic (RBC) Canlı Fiyat Grafiği

Sorumluluk Reddi: Bu sitede yeniden yayınlanan makaleler, halka açık platformlardan alınmıştır ve yalnızca bilgilendirme amaçlıdır. MEXC'nin görüşlerini yansıtmayabilir. Tüm hakları telif sahiplerine aittir. Herhangi bir içeriğin üçüncü taraf haklarını ihlal ettiğini düşünüyorsanız, kaldırılması için lütfen service@support.mexc.com ile iletişime geçin. MEXC, içeriğin doğruluğu, eksiksizliği veya güncelliği konusunda hiçbir garanti vermez ve sağlanan bilgilere dayalı olarak alınan herhangi bir eylemden sorumlu değildir. İçerik, finansal, yasal veya diğer profesyonel tavsiye niteliğinde değildir ve MEXC tarafından bir tavsiye veya onay olarak değerlendirilmemelidir.

Ayrıca Şunları da Beğenebilirsiniz

The Channel Factories We’ve Been Waiting For

The post The Channel Factories We’ve Been Waiting For appeared on BitcoinEthereumNews.com. Visions of future technology are often prescient about the broad strokes while flubbing the details. The tablets in “2001: A Space Odyssey” do indeed look like iPads, but you never see the astronauts paying for subscriptions or wasting hours on Candy Crush. Channel factories are one vision that arose early in the history of the Lightning Network to address some challenges that Lightning has faced from the beginning. Despite having grown to become Bitcoin’s most successful layer-2 scaling solution, with instant and low-fee payments, Lightning’s scale is limited by its reliance on payment channels. Although Lightning shifts most transactions off-chain, each payment channel still requires an on-chain transaction to open and (usually) another to close. As adoption grows, pressure on the blockchain grows with it. The need for a more scalable approach to managing channels is clear. Channel factories were supposed to meet this need, but where are they? In 2025, subnetworks are emerging that revive the impetus of channel factories with some new details that vastly increase their potential. They are natively interoperable with Lightning and achieve greater scale by allowing a group of participants to open a shared multisig UTXO and create multiple bilateral channels, which reduces the number of on-chain transactions and improves capital efficiency. Achieving greater scale by reducing complexity, Ark and Spark perform the same function as traditional channel factories with new designs and additional capabilities based on shared UTXOs. Channel Factories 101 Channel factories have been around since the inception of Lightning. A factory is a multiparty contract where multiple users (not just two, as in a Dryja-Poon channel) cooperatively lock funds in a single multisig UTXO. They can open, close and update channels off-chain without updating the blockchain for each operation. Only when participants leave or the factory dissolves is an on-chain transaction…

Paylaş

BitcoinEthereumNews2025/09/18 00:09

SOLANA NETWORK Withstands 6 Tbps DDoS Without Downtime

The post SOLANA NETWORK Withstands 6 Tbps DDoS Without Downtime appeared on BitcoinEthereumNews.com. In a pivotal week for crypto infrastructure, the Solana network

Paylaş

BitcoinEthereumNews2025/12/16 20:44

Crucial Fed Rate Cut: October Probability Surges to 94%

BitcoinWorld Crucial Fed Rate Cut: October Probability Surges to 94% The financial world is buzzing with a significant development: the probability of a Fed rate cut in October has just seen a dramatic increase. This isn’t just a minor shift; it’s a monumental change that could ripple through global markets, including the dynamic cryptocurrency space. For anyone tracking economic indicators and their impact on investments, this update from the U.S. interest rate futures market is absolutely crucial. What Just Happened? Unpacking the FOMC Statement’s Impact Following the latest Federal Open Market Committee (FOMC) statement, market sentiment has decisively shifted. Before the announcement, the U.S. interest rate futures market had priced in a 71.6% chance of an October rate cut. However, after the statement, this figure surged to an astounding 94%. This jump indicates that traders and analysts are now overwhelmingly confident that the Federal Reserve will lower interest rates next month. Such a high probability suggests a strong consensus emerging from the Fed’s latest communications and economic outlook. A Fed rate cut typically means cheaper borrowing costs for businesses and consumers, which can stimulate economic activity. But what does this really signify for investors, especially those in the digital asset realm? Why is a Fed Rate Cut So Significant for Markets? When the Federal Reserve adjusts interest rates, it sends powerful signals across the entire financial ecosystem. A rate cut generally implies a more accommodative monetary policy, often enacted to boost economic growth or combat deflationary pressures. Impact on Traditional Markets: Stocks: Lower interest rates can make borrowing cheaper for companies, potentially boosting earnings and making stocks more attractive compared to bonds. Bonds: Existing bonds with higher yields might become more valuable, but new bonds will likely offer lower returns. Dollar Strength: A rate cut can weaken the U.S. dollar, making exports cheaper and potentially benefiting multinational corporations. Potential for Cryptocurrency Markets: The cryptocurrency market, while often seen as uncorrelated, can still react significantly to macro-economic shifts. A Fed rate cut could be interpreted as: Increased Risk Appetite: With traditional investments offering lower returns, investors might seek higher-yielding or more volatile assets like cryptocurrencies. Inflation Hedge Narrative: If rate cuts are perceived as a precursor to inflation, assets like Bitcoin, often dubbed “digital gold,” could gain traction as an inflation hedge. Liquidity Influx: A more accommodative monetary environment generally means more liquidity in the financial system, some of which could flow into digital assets. Looking Ahead: What Could This Mean for Your Portfolio? While the 94% probability for a Fed rate cut in October is compelling, it’s essential to consider the nuances. Market probabilities can shift, and the Fed’s ultimate decision will depend on incoming economic data. Actionable Insights: Stay Informed: Continue to monitor economic reports, inflation data, and future Fed statements. Diversify: A diversified portfolio can help mitigate risks associated with sudden market shifts. Assess Risk Tolerance: Understand how a potential rate cut might affect your specific investments and adjust your strategy accordingly. This increased likelihood of a Fed rate cut presents both opportunities and challenges. It underscores the interconnectedness of traditional finance and the emerging digital asset space. Investors should remain vigilant and prepared for potential volatility. The financial landscape is always evolving, and the significant surge in the probability of an October Fed rate cut is a clear signal of impending change. From stimulating economic growth to potentially fueling interest in digital assets, the implications are vast. Staying informed and strategically positioned will be key as we approach this crucial decision point. The market is now almost certain of a rate cut, and understanding its potential ripple effects is paramount for every investor. Frequently Asked Questions (FAQs) Q1: What is the Federal Open Market Committee (FOMC)? A1: The FOMC is the monetary policymaking body of the Federal Reserve System. It sets the federal funds rate, which influences other interest rates and economic conditions. Q2: How does a Fed rate cut impact the U.S. dollar? A2: A rate cut typically makes the U.S. dollar less attractive to foreign investors seeking higher returns, potentially leading to a weakening of the dollar against other currencies. Q3: Why might a Fed rate cut be good for cryptocurrency? A3: Lower interest rates can reduce the appeal of traditional investments, encouraging investors to seek higher returns in alternative assets like cryptocurrencies. It can also be seen as a sign of increased liquidity or potential inflation, benefiting assets like Bitcoin. Q4: Is a 94% probability a guarantee of a rate cut? A4: While a 94% probability is very high, it is not a guarantee. Market probabilities reflect current sentiment and data, but the Federal Reserve’s final decision will depend on all available economic information leading up to their meeting. Q5: What should investors do in response to this news? A5: Investors should stay informed about economic developments, review their portfolio diversification, and assess their risk tolerance. Consider how potential changes in interest rates might affect different asset classes and adjust strategies as needed. Did you find this analysis helpful? Share this article with your network to keep others informed about the potential impact of the upcoming Fed rate cut and its implications for the financial markets! To learn more about the latest crypto market trends, explore our article on key developments shaping Bitcoin price action. This post Crucial Fed Rate Cut: October Probability Surges to 94% first appeared on BitcoinWorld.

Paylaş

Coinstats2025/09/18 02:25